The UK based publication Middle East Eye has reported that the recent crash in oil prices happened due to a row between Saudi Crown prince Muhammad Bin Salman and the Russian President Vladimir Putin over a phone call that ended “badly”. Thus followed a series of events that has left the global oil industry shaking.

The UK based publication Middle East Eye has reported that the recent crash in oil prices happened due to a row between Saudi Crown prince Muhammad Bin Salman and the Russian President Vladimir Putin over a phone call that ended “badly”. Thus followed a series of events that has left the global oil industry shaking.The call took before OPEC+ meeting on March 6 that proposed cutting down production but was not agreed upon as Russia dissented. According to the MEE exclusive report: “Just before that meeting there was a call between Putin and MBS. MBS was very aggressive and gave an ultimatum. He threatened that if there is no agreement, Saudi would start a price war. The conversation was very personal. They shouted at each other. Putin refused the ultimatum and the call ended badly, the Saudi official said, speaking on condition of anonymity.” The experts have been terming it a "bold, unprecedented gambit".

Given the corona pandemic led fall in demand for oil, cutting down production by 1.5m barrels a day was proposed. Later, Saudi Arabia started to flood the oil markets in a failed bid to “corner” Putin. However, Saudi Arabia’s USD100 billion worth oil supply is a gambit that could backfire with devastating consequences for the KSA economy.

The U.S. President Donald Trump initially hailed the fall in prices but as the crude oil producers from Texas expressed their concern, the situation became complicated.

The U.S. is considering to halt import of Saudi oil to protect its domestic oil industry. Meanwhile, countries like Canada and Indonesia are storing the cheap oil for future. Developing countries view price fall as a positive shock as their import bill would drastically reduce, thereby, stabilizing current account and trade deficits.

The U.S. is considering to halt import of Saudi oil to protect its domestic oil industry. Meanwhile, countries like Canada and Indonesia are storing the cheap oil for future. Developing countries view price fall as a positive shock as their import bill would drastically reduce, thereby, stabilizing current account and trade deficits.About three-months after Iranian attacks on Aramco, a void was visible in Middle East and Russia sought to fulfill it by strengthening ties with Saudi Arabia, offering missile defense system advanced in comparison to S-300 sold to Iran and S-400 sold to Turkey. However, there could not be a formal contract signing. And then, the row between MBS and Putin happened over the phone.

“By the time Saudi Arabia sought a new partner in Russia, Dmitriev –– CEO of Russia’s sovereign wealth fund RDIF –– had key credentials to conduct negotiations with Saudi Arabia and bin Salman personally. These ties were cemented in a bizarre ceremony in which Dmitriev was awarded the Order of King Abdulaziz, the highest civilian honour in the kingdom, Dmitriev later played a key role in securing a Russian-Saudi agreement on oil, announced on 12 April, when OPEC+ finally agreed to reduce global production by about 10 percent,” stated the MiddleEastEye.

“By the time Saudi Arabia sought a new partner in Russia, Dmitriev –– CEO of Russia’s sovereign wealth fund RDIF –– had key credentials to conduct negotiations with Saudi Arabia and bin Salman personally. These ties were cemented in a bizarre ceremony in which Dmitriev was awarded the Order of King Abdulaziz, the highest civilian honour in the kingdom, Dmitriev later played a key role in securing a Russian-Saudi agreement on oil, announced on 12 April, when OPEC+ finally agreed to reduce global production by about 10 percent,” stated the MiddleEastEye.Saudi Arabia's economy was already struggling, growing by just 0.3 percent last year. The annual Hajj and Umrah pilgrimages are major contributors to Saudi Arabia's economy, attracting close to 10 million pilgrims per year and generating over $8B in revenues. Given the COVID-19 pandemic, Umrah remains suspended while the Hajj could also be cancelled as Saudi officials have been urging Muslims to consider postponing the pilgrimage untill the pandemic is under control. This would add to annual financial losses.

The economic state of Saudi Arabia would have dire consequences on other Gulf states while the relations of the Kingdom with other states would be severely affected. "Since the last oil price cut [in 2014], the GCC has burned through foreign reserves, but they rode it out. The discussion now is that they can't do it this time", warned adjunct professor Vesalius College Guy Burton.

The GCC's finances have become so perilous that the International Monetary Fund warned in a February report that "the region's aggregate net financial wealth, estimated at $2 trillion at present, would turn negative by 2034 as the region becomes a net borrower."

In 1985, US vice president George HW Bush visited Saudi Arabia to pressure the kingdom to flood the global market with cheap oil and squeeze the energy revenues of the Soviet Union. Fast forward to March 2020, and an oil price war is being played once again, with consequences for Washington, Moscow and the entire global economy.

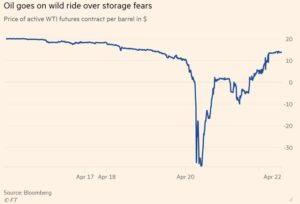

As Saudi Arabia clashed with Russia over oil prices, the Kingdom raised production to 13 million barrels per day. Consequently, as of April 22, the supply glut led prices fell by 30% this week; 17% in Asia to $15.98 a barrel while $19 a barrel in Europe, reported Financial Times. Meanwhile, the storage capacity has been struggling to catch up, "floating storage had risen by 120 per cent in the past eight weeks to a record high of more than 120m barrels," said Robert Rennie, global head of market strategy at Westpac.